Assessing Progress in Sustainable Governance: Results of the most recent Sustainable Governance Indicators Survey

12 June 2025

Research and Deployment of Transformation Policies

19 June 2025

By Darina DAKMAK, Florian PILEYRE and Egor POLISHCHUK

I. Introduction

In the Commission’s Communication about the European Green Deal issued in 2019, the intention of cooperating with the world in order to achieve the green transition was made very clear: “the environmental ambition of the Green Deal will not be achieved by Europe acting alone”.[1] To this day, the European Green Deal objectives are closely linked to that of the 2015 Paris Agreement, illustrating the EU’s will to pursue broader cooperation with like-minded partners on the path to transition. However, with the multiple supply chain crises caused by the Covid pandemic, Russia’s attempt at hindering the EU’s support to Ukraine by using its dependency on Russian oil and gas supply, as well as the perspective of a new dependency upon China for critical raw materials necessary for the transition, debates arose about whether it would might actually be safer for Europe to achieve the said transition by eliminating risky dependencies and risky supply chains. [2][3][4][5]

The concept of de-risking, when applied to the EU supply chains, can mean three things. First, it can mean supply chain internalisation, meaning that a given supply chain which previously included non-EU partners becomes entirely located on EU territory and thus entirely controllable. Secondly, it can mean supply chain relocalization, where the EU replaces its previous foreign partner in a given supply chain by another, following a geographical logic (making the supply chain shorter) or a friendshoring one (making the supply chain less prone to political blackmail). Thirdly, it can mean diversification, where the EU multiplies import partners in order to not be overly dependent on imports from only one partner. In all of these cases, the goal would be to make the supply chain less risky, either by reducing its disruption probability in case of a Covid-type crisis, or by reducing its chances of being used as a means of geopolitical leverage on the EU in case of a Russia-Ukraine-type conflict. Thus, the de-risking of supply chains implies a security dimension which was not thought of in the initial design of the European Green Deal.

However, integrating a security component into the Green Deal couldn’t mean making Europe’s path to transition isolated from the rest of the world, first because of the EU’s historical reliance on free trade, and secondly because climate change as a global problem could not be efficiently tackled on an exclusively regional level. The main interrogation of our blog would thus be the following: how and to what extent can the EU Green Deal help mitigate the geopolitical, technological and economic risks to its supply chains as part of its de-risking strategy?

We will first carve out an outline of the EU’s de-risking strategy, then study the implementation of the Green Deal strategy in regards to de-risking, and finally see to what extent the Green Deal is able to achieve its de-risking goals.

II. The EU de-risking strategy in the EU Green deal: key sectors, policies, and goals

Following the launch of the Russian full-scale invasion in Ukraine, the European Green Deal took on a new dimension. From then on, the argument in favour of more renewables in the energy mix wouldn’t be only economic or ideological, but also a security one.[6] In the face of the Russian oil and gas blackmail attempt, Europe made the choice of accelerating the green transition in its energy mix, while looking for substitutes for Russian hydrocarbons in the short term. Energy was thus identified as a key vulnerable sector targeted by the European Green Deal. The increase of renewables in the energy mix acted as an internalisation factor in the energy supply chain, while the research of new hydrocarbon import partners (the main of which happened to be the US and Norway, two democracies and NATO members) acted as a relocalization and diversification factor.[7]

Another crucial domain for the European Green Deal objectives, raw materials, has also quickly been identified as a vulnerable supply chain.[8] The raw materials supply chain was indeed very similar to the energy supply chain which existed before 2022, only in this case the main partner of the EU wasn’t Russia but China.[9] In a context of growing tensions between China and Taiwan, de-risking the raw materials supply chain progressively became one of the most important security priorities which the European Green Deal could cover. For example, magnesium, the use of which allows environmental gains in aviation as well as a reduction in fuel consumption for automobiles, is almost totally imported from China. In the same vein, all the rare earths used to make magnets, used for example in electric motors, are refined in the People’s Republic. Other raw material supply chains are also undiversified and overly reliant on imports from a few countries, which are not necessarily the most safe (for example the DR Congo, in which 63% of the world’s cobalt is extracted) or the most reliable partners (for example Turkey, from which the EU imports 98% of its borate).[10]

For the energy sector, the RePowerEU plan had a goal to diversify energy supplies and produce more clean energy.[11] More than two years after its implementation, Russian gas supply represents only 15% of all gas imported by the EU and more energy has been produced from wind and solar than from gas in the EU in 2023. Thus, the EU’s energy supply chain has been considerably internalised (by the increased use of renewables), relocalized (from Russia) and diversified (with new major import partners such as the US and Norway, and with more diverse national energy mixes). However, the biggest threat to the European energy supply chain remains the fragmentation of the European electricity market, which leads to the duplication of energy capacities and to the suboptimal use of the Member States’ energy potential.[12]

For the raw materials sector, a Critical Raw Materials Act has been adopted as a part of the EU Green Deal Industrial Plan. The goal of the act is to internalise as much as possible the raw materials supply chain, but especially to diversify it. By 2030, European domestic capacities must be able to satisfy 10% of the EU’s annual needs for extraction; 40% for processing and 25% for recycling. Moreover, no more than 65% of the EU’s annual needs of each critical raw material at any of the mentioned stages should come from a single third country.

III. Feasibility of implementing EUGD policies with regards to derisking

Comparison of easy to de risk-sectors vs hard to de-risk sectors

Speeches about ramping up the EU strategic autonomy can be quite different in acts and implementation. This is because in the EU’s de-risking strategy, certain critical sectors are easier to insulate from global dependencies than others due to varying levels of existing infrastructure, access to raw materials, and technological maturity.

One of the most significant strategies in recent years has been the reduction of dependence on Russian fossil fuels since the onset of the Russian aggression in Ukraine. With RePowerEU, the EU has significantly decreased its reliance on Russian energy and has become more energy independent. This has been primarily implemented with import bans, a relocation and diversification of supply sources (e.g. towards the US, Norway etc.) as well as RePowerEU’s efforts to increase the share of renewable energy.

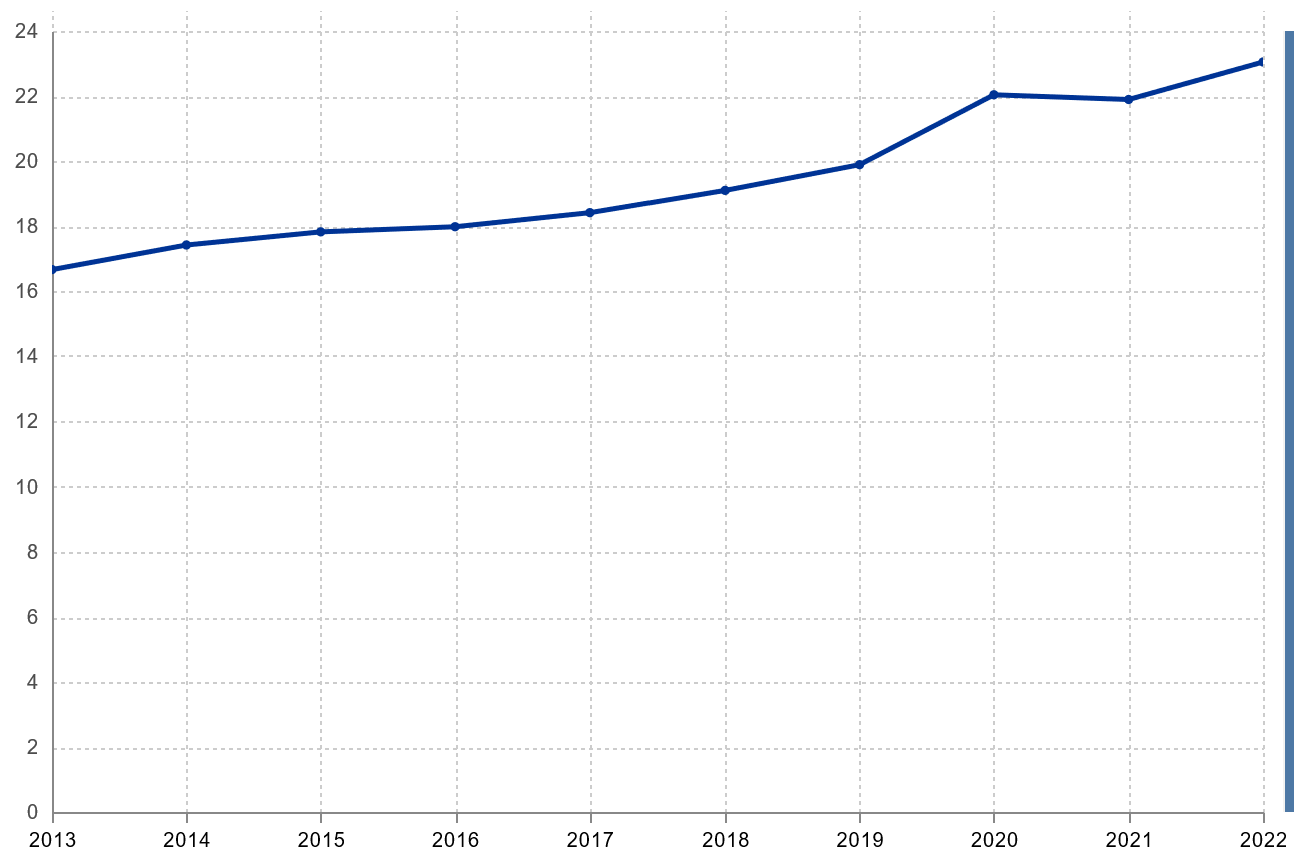

But overall, the energy sector could be considered as easier to de-risk due to the strong existing capacities and infrastructures of member states. The commitment to expanding solar, wind, and other renewable sources also contributes to this. Indeed, reducing the risks associated with energy dependency has a solid regulatory framework and a long-standing commitment: the Energy Union Strategy of 2015 and the successive legislative packages of the European Green Pact (Fit for 55 package, EU Renewable Energy directive). As shown in the graph, the different legislative packages of the Green Deal have shown substantial progress in renewable energy. They however create new dependencies on critical materials, semiconductors and strategic technologies necessary for production of renewable infrastructure. These are harder to de-risk as they rely more on globalised supply chain complexities.[5]

One of the most challenging areas is the semiconductor industry. Semiconductors are crucial components in countless modern technologies, from smartphones to renewable energy systems. For instance, semiconductors play an essential role in solar panels, where they convert sunlight into electricity. The EU currently relies heavily on imports from Asia, particularly China, Taiwan and South Korea, which dominate global semiconductor production. To address this dependency, the EU has introduced initiatives like the European Chips Act.[14] However, achieving independence in this highly complex, technology-driven sector is a long-term endeavour that will require substantial investment and innovation.

Another pressing area involves critical raw materials — specifically lithium, cobalt, and rare earth elements. These materials are indispensable in various advanced industries, including electric vehicle batteries and electronics. However, the EU remains significantly dependent on imports, especially from China, to meet its demand for these resources. This reliance complicates efforts to establish secure and sustainable supply chains. Efforts to develop domestic sources and recycling programs are ongoing but will take time to materialise.

For those key areas, the EU has developed a 5 pillar strategy with which it aims to overcome its high dependency in the middle to long term: (1) making EU industries more competitive and resilient (2) reduce commercial distortion with adequate regulatory framework (3) Defend criticals sectors like robotics or AI (4) boosting new free trade deals and partnerships to diversify supply chains and (5) putting the emphasis on recycling.

First, the EU is focused on enhancing the competitiveness and resilience of its industries through digitalization and the green transition. These dual priorities aim to strengthen the industrial base while ensuring alignment with global sustainability objectives.

A key element of this approach includes leveraging existing trade rules to minimise market distortions and enhance security in critical technologies, such as 5G. To reinforce economic security and maintain a level playing field, particularly in relation to major global competitors such as China, the EU has introduced several regulatory measures. These include the Foreign Direct Investment Screening Framework, the Foreign Subsidies Regulation, the Carbon Border Adjustment Mechanism (CBAM), and the Anti-Coercion Instrument. These tools are designed to safeguard strategic sectors and ensure fair competition.[5]

Because the EU’s de-risking strategy aims to defend critical sectors like robotics, artificial intelligence (AI), and semiconductors to boost resilience and reduce dependency on non-European suppliers. Those technologies are vital for enabling the green transition across industries such as manufacturing, agriculture, and transportation by enhancing resource efficiency, reducing emissions, and improving productivity. A cornerstone of this approach is the European Chips Act, by investing in chip manufacturing and innovation, the EU aims to double its global market share in semiconductors by 2030, supporting the strategic autonomy needed to secure other high-tech sectors.

Diversifying supply chain partners is another priority, especially given the projected 500% increase in demand for critical raw materials by 2050, as reported by the World Bank.[15] To mitigate these dependencies, the EU’s Global Gateway strategy facilitates supply chain diversification through strategic partnerships and free trade agreements (11 formed partnerships as of today including Chile, Ukraine, Congo, Rwanda, known as “raw materials diplomacy”).[16] Through these partnerships, the EU not only secures essential materials for green technologies but also fosters resilience in its supply chain by investing in sustainable infrastructure and technology in partner nations, laying a foundation for stable, long-term resource flows. This strategy allows the EU to protect its interests in critical sectors while promoting fair trade practices.

Finally, rather than looking only for new suppliers, the EU can reduce its dependence by recycling its waste. By focusing on innovation and research, one of the solutions identified by the European Commission is to eventually be able to re-use as many critical materials as possible from waste. The Critical Raw Materials Act (CRMA), includes a target of 25% of the EU’s annual CRM consumption should come from recycling by 2030.[10] End-of-Life Vehicles directive can also be cited (ensure that at least 25% of plastic used to build a vehicle comes from recycling).[17]

IV. How and to what extent can the EU Green Deal help mitigate the geopolitical, technological and economic risks to its supply chains as part of its de-risking strategy?

“Our relations are not black or white – and our response cannot be either. This is why we need to focus on de-risk – not de-couple”.[18] These were the words pronounced by Ursula von der Leyen during a speech on EU-China relations in 2023. By underscoring the idea that there is no intent to “de-couple”, the EU’s de-risking strategy displays the importance of keeping a reasonable balance in the path towards reduction of dependencies. This approach aims “to find a better equilibrium between seizing opportunities and managing risks”.[19] Indeed, engaging in de-risking unveils a multiplicity of challenges.

According to the European Council on Foreign Relations (ECFR), the consequences of de-risking should be assessed through security, economic and climate factors, forming a triangle whose structure is greatly impacted by decisions taken on each side : “Shrink the exposure along one side of the triangle, and risks will grow along another side.” [20]

On the economic front, by drifting away from markets conferring cheaper imports of raw materials, the EU will have to take into account the emergence of supplementary costs, which could impact its competitiveness and also slow down the green transition.[21] In terms of cost competitiveness for the production of solar panels for instance, it is estimated that EU’s supplies would be 35% more expensive than imports.[22] It has also been argued that the EU’s de-risking strategy fails to properly address “disruptions to exports, which could equally have a macroeconomic impact if they were highly concentrated in any one destination country”.[21]

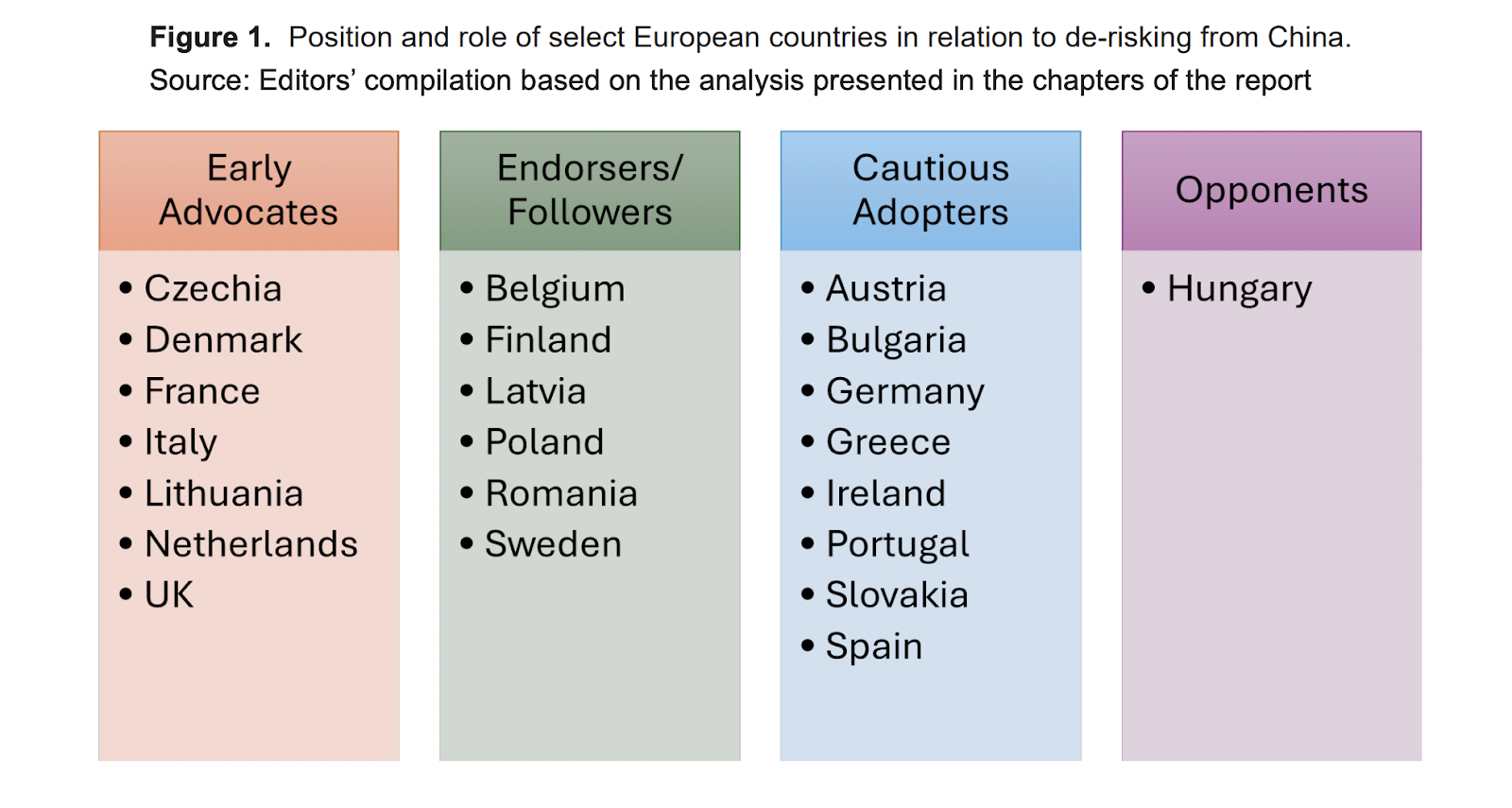

Other challenges pointed out are the increased vulnerability to “domestic shocks (…) whose consequences would be mitigated by international trade and/or capital flows” and a rise in consumer prices.[21] Widening disparities may also arise across EU countries. The de-risking process faces a lack of consensus within the European Union due to the diversity of member states’ interests, depending on their level of reliance on imports. Therefore, the scope of the de-risking strategy may be a source of divisions as “smaller EU members with little to lose are willing to go further than their larger Western neighbours”.[23]

According to the EPRS, the complexity of formulating policy responses for de-risking and the perspective of “slow political decision-making” should be considered as a proper risk.[24] De-risking also brings coordination challenges as supply chains differ greatly from one another, thus highlighting possible efficiency issues. Furthermore, the geopolitical context is determining when evaluating the implications of de-risking. The EU’s diversification strategy relies heavily “on the openness of the global trade system”, such an approach is thus subject to inherent fragilities under tense circumstances.[24]

Nevertheless, de-risking remains determinant for the EU’s autonomy, resilience and ability to strengthen its leadership position. When analysing costs and benefits of the de-risking strategy, a gradual de-risking is considered to be a safer approach for the EU’s economy, with potential costs being lower.[25]

Regarding the EU’s energy transition, the evaluation of costs emerging from de-risking should also be balanced with the extent to which this strategy acts as a safety net. Through greater resilience, the EU can prevent having to deal with unexpected cost increases in case of “possible disruption to the energy transition to renewables”.[21] In the long term, the de-risking strategy allows the EU to face the future more serenely, with more stability, visibility and control over its development ambitions.

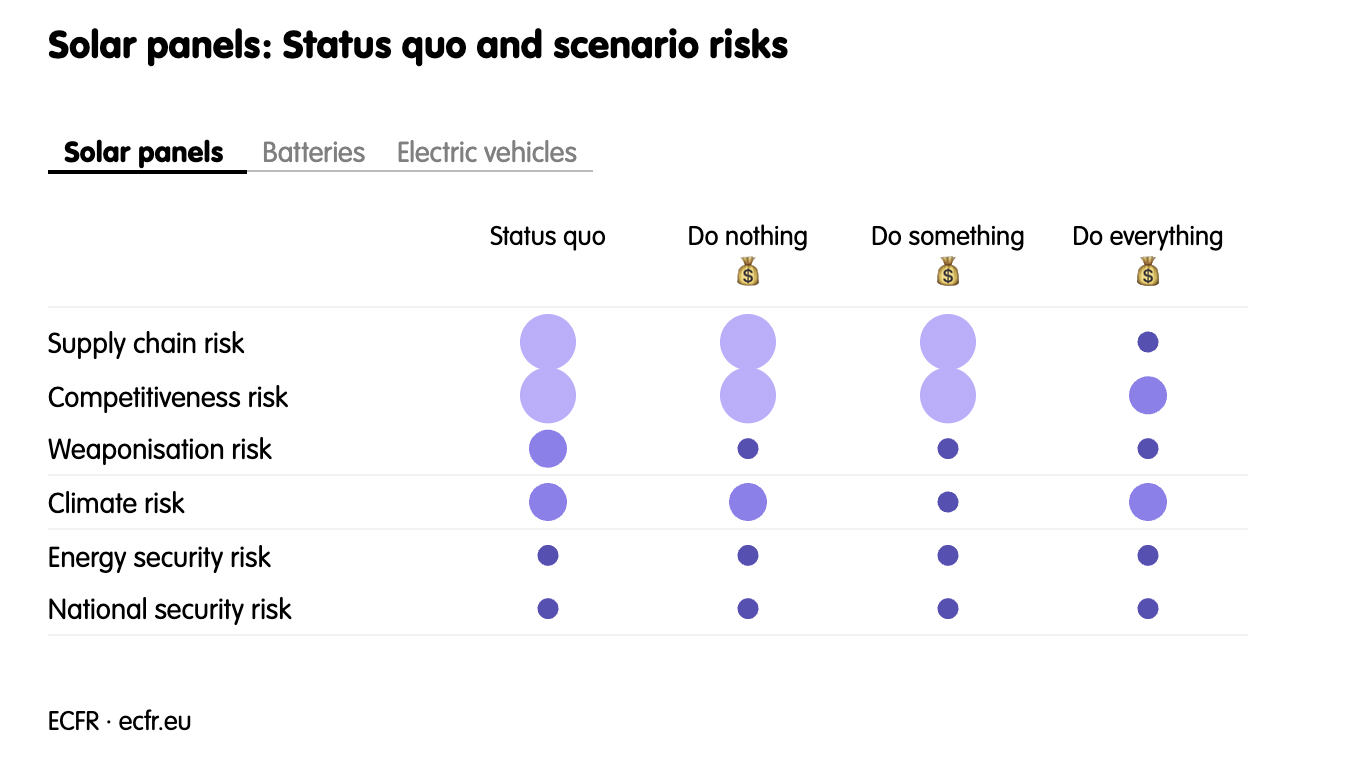

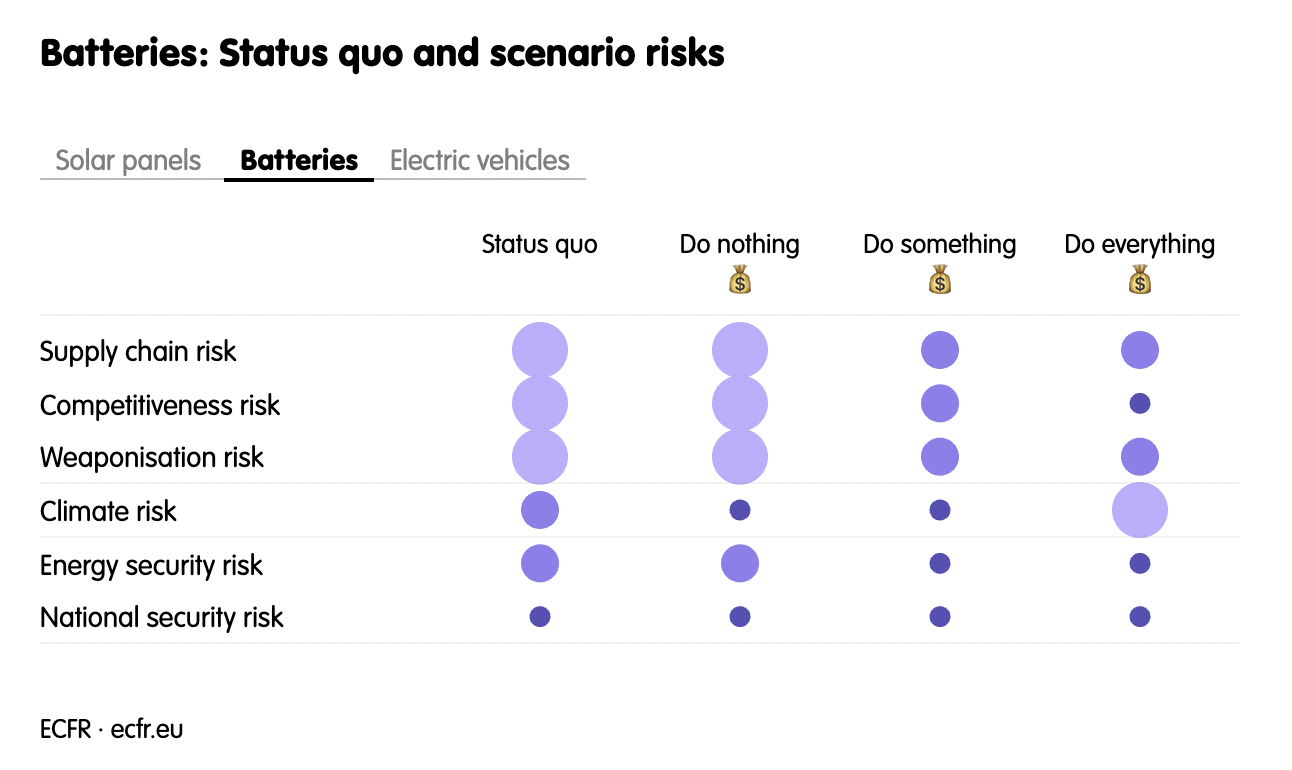

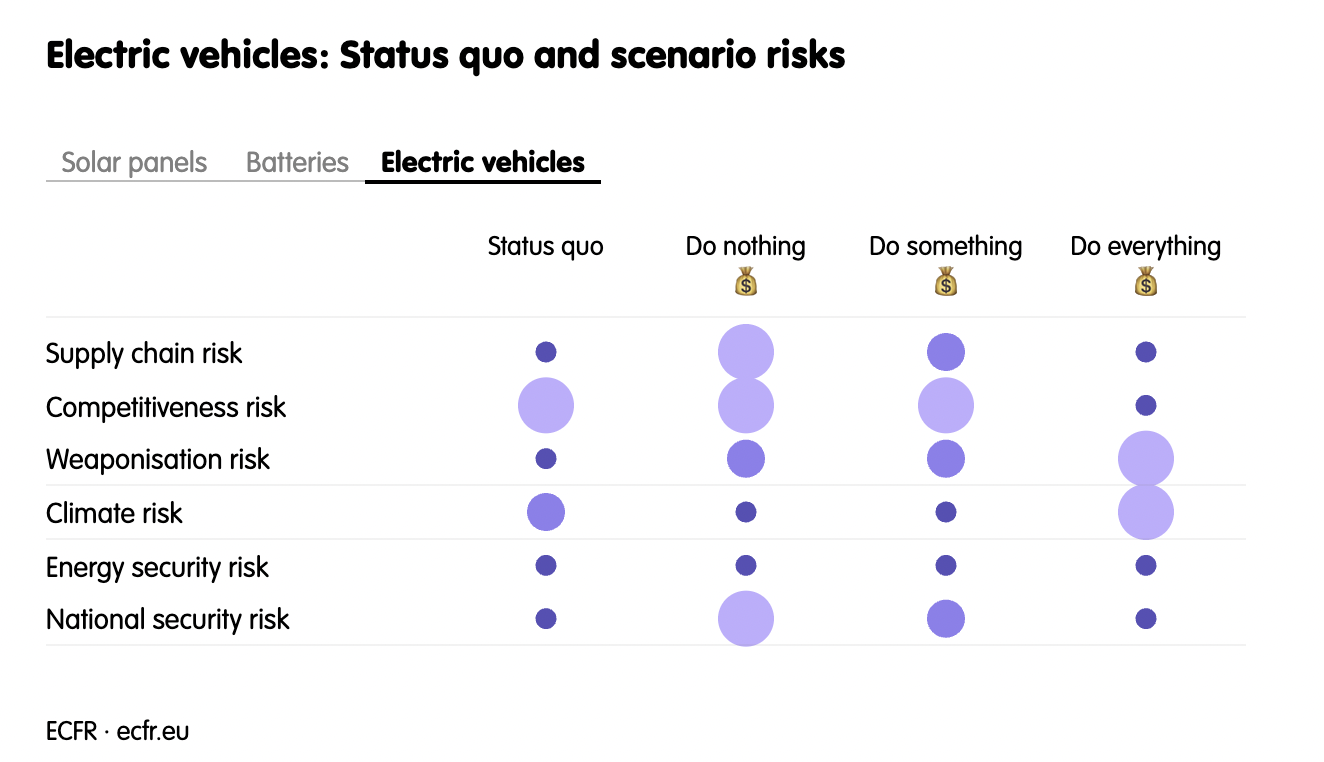

By increasing its domestic capacity, the EU takes essential steps towards the achievement of Green Deal objectives, insuring against a weaponization of supplies which would be detrimental to the transition.[26] De-risking is associated with leverage and deterrence effects. Moreover, exploring the different ECFR scenarios of EU’s strategic approach towards China for reliance on solar panels, batteries and electric vehicles, it is possible to point out that de-risking, despite its costs, leads to less drawbacks than keeping the “current state of play in crucial green industrial sectors”.[20]

Additionally, considering the difference in interests and perceptions of risks between the EU and firms (noting that private enterprises are key actors controlling important supply chains), policy-led de-risking may be deemed as necessary in order to avoid potentially jeopardising situations (firms neglecting what should be considered as threats for EU’s supply chains) for the society as a whole.[21][24]

It is worth reminding that through de-risking, the EU also has opportunities to foment coordination with other economies “including the US but also many emerging economies, whose energy transition depends on China”, which could therefore lead to reduced costs.[27] Therefore, while de-risking entails geopolitical risks in case of escalating tensions, one should also consider that turning to large and diversified partnerships could also provide the EU with better abilities to respond to challenges along the path. The process of de-risking is one of trade-offs, and it is a lengthy movement which implies a full-fledged industrial development.[28]

The goals of the European Green Deal, with the measures established, align in the long-term with the EU’s pursuit of de-risking. When aiming for diversification, the EU can rely on the Green Deal framework to limit threats of overdependence through funds available, alliances, regulatory tools, incentives to foster research and technological innovation.

Overall, economic and political risks induced by the EU’s de-risking strategy are not insurmountable barriers. De-risking supply chains is necessary for the EU’s ambitions in the long-term and will be an important step-up for the objectives set in order to reach a climate-neutral Europe. However, the EU’s capacity to speak with one voice will be vital to ensure that benefits to come will overpower predicted challenges during the implementation phase of this strategy.

V. Bibliography

[1] European Commission, “COM/2019/640 final, COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT, THE EUROPEAN COUNCIL, THE COUNCIL, THE EUROPEAN ECONOMIC AND SOCIAL COMMITTEE AND THE COMMITTEE OF THE REGIONS The European Green Deal.” Accessed: Nov. 08, 2024. [Online]. Available: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A52019DC0640

[2] M. G. Attinasi, M. Balatti, M. Mancini, and L. Metelli, “Supply chain disruptions and the effects on the global economy,” Jan. 2022, Accessed: Nov. 08, 2024. [Online]. Available: https://www.ecb.europa.eu/press/economic-bulletin/focus/2022/html/ecb.ebbox202108_01~e8ceebe51f.en.html

[3] D. Frum, “Why Putin’s Secret Weapon Failed,” The Atlantic. Accessed: Nov. 08, 2024. [Online]. Available: https://www.theatlantic.com/ideas/archive/2023/06/russia-ukraine-natural-gas-europe/674268/

[4] I. Johnston, A. Hancock, and H. Dempsey, “Can Europe go green without China’s critical minerals?” Accessed: Nov. 08, 2024. [Online]. Available: https://ig.ft.com/ig-rare-earths

[5] EPRS, “Future Shocks 2023: De-risking Europe’s global critical supply chains [Policy podcast].” Accessed: Nov. 08, 2024. [Online]. Available: https://epthinktank.eu/2023/08/18/future-shocks-2023-de-risking-europes-global-critical-supply-chains/

[6] Geoffroy Dolphin, Romain Duval, Galen Sher, and Hugo Rojas-Romagosa, “Europe Can Reap Sizable Energy Security Rewards by Scaling Up Climate Action,” IMF. Accessed: Nov. 08, 2024. [Online]. Available: https://www.imf.org/en/Blogs/Articles/2024/05/29/europe-can-reap-sizable-energy-security-rewards-by-scaling-up-climate-action

[7] Victoria Zaretskaya, “The United States remained the largest liquefied natural gas supplier to Europe in 2023 – U.S. Energy Information Administration,” EIA. Accessed: Nov. 08, 2024. [Online]. Available: https://www.eia.gov/todayinenergy/detail.php?id=61483

[8] Eurostat, “Critical raw materials and their supply risk.” Accessed: Nov. 08, 2024. [Online]. Available: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=File:Critical_raw_materials_and_their_supply_risk.png

{kind=link}

[9] European Commission, “RMIS – Critical, strategic and advanced materials,” RMIS – Raw Materials Information System. Accessed: Nov. 08, 2024. [Online]. Available: https://rmis.jrc.ec.europa.eu/eu-critical-raw-materials

[10] European Commission, “European Critical Raw Materials Act.” Accessed: Nov. 08, 2024. [Online]. Available: https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/european-green-deal/green-deal-industrial-plan/european-critical-raw-materials-act_en

[11] European Commission, “REPowerEU.” Accessed: Nov. 08, 2024. [Online]. Available: https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/european-green-deal/repowereu-affordable-secure-and-sustainable-energy-europe_en

[12] European Commission, “Reform of the EU electricity market design,” European Commission – European Commission. Accessed: Nov. 08, 2024. [Online]. Available: https://ec.europa.eu/commission/presscorner/detail/en/ip_23_1591

[13] M. Draghi, “The Future of European competitiveness Part B | In-depth analysis and recommendations,” 2024. [Online]. Available: https://commission.europa.eu/document/download/ec1409c1-d4b4-4882-8bdd-3519f86bbb92_en?filename=The%20future%20of%20European%20competitiveness_%20In-depth%20analysis%20and%20recommendations_0.pdf

[14] European Commission, “European Chips Act.” Accessed: Nov. 08, 2024. [Online]. Available: https://commission.europa.eu/strategy-and-policy/priorities-2019-2024/europe-fit-digital-age/european-chips-act_en

[15] World Bank, “Climate-Smart Mining: Minerals for Climate Action,” World Bank. Accessed: Nov. 08, 2024. [Online]. Available: https://www.worldbank.org/en/topic/extractiveindustries/brief/climate-smart-mining-minerals-for-climate-action

[16] European Commission, “Raw materials diplomacy – European Commission.” Accessed: Nov. 08, 2024. [Online]. Available: https://single-market-economy.ec.europa.eu/sectors/raw-materials/areas-specific-interest/raw-materials-diplomacy_en

[17] European Commission, “End-of-Life Vehicles.” Accessed: Nov. 08, 2024. [Online]. Available: https://environment.ec.europa.eu/topics/waste-and-recycling/end-life-vehicles_en

[18] European Commission, “Speech by President von der Leyen on EU-China relations to the Mercator Institute for China Studies and the European Policy Centre”, 30 March, 2023, https://ec.europa.eu/commission/presscorner/detail/en/speech_23_2063

[19] European Parliament, “EU-China relations: De-risking or de-coupling − the future of the EU strategy towards China”, March 2024, https://www.europarl.europa.eu/RegData/etudes/STUD/2024/754446/EXPO_STU(2024)754446_EN.pdf

[20] Lipke, Alexander, Oertel, Janka, O’Sullivan, Daniel, “Trust and trade-offs: How to manage Europe’s green technology dependence on China”, ECFR, 29 May 2024, https://ecfr.eu/publication/trust-and-trade-offs-how-to-manage-europes-green-technology-dependence-on-china/

[21] Pisani-Ferry, Jean, Weder di Mauro, Beatrice, Zettelmeyer Jeronym, “How to de-risk: European economic security in a world of interdependence”, Bruegel, 7 May 2024, https://www.bruegel.org/policy-brief/how-de-risk-european-economic-security-world-interdependence

[22] Gros, Daniel, “Geopolitics and the De-Risking of Trade”, Bocconi, Accessed: 13 November 2024, https://iep.unibocconi.eu/publications/geopolitics-and-de-risking-trade

[23] MERICS, “Expert debate on: What does it really mean for Europe to ‘de-risk’ its relationship with China?”, 4 January 2024, https://merics.org/en/comment/expert-debate-what-does-it-really-mean-europe-de-risk-its-relationship-china

[24] EPRS Strategic Foresight and Capabilities Unit, “Future Shocks 2023: De-risking Europe’s global critical supply chains [Policy podcast]”, EPRS, 18 August 2023, https://epthinktank.eu/2023/08/18/future-shocks-2023-de-risking-europes-global-critical-supply-chains/

[25] Baqaee, David, Hinz, Julian, Moll, Benjamin, Schularick, Moritz, Teti, Feodora A., Wanner, Joschka, Yang, Sihwan, “What if? The effects of a hard decoupling from China on the German economy”, CEPR Paris Symposium, December 2023, https://benjaminmoll.com/wp-content/uploads/2023/12/what_if_china.pdf

[26] García-Herrero, Alicia, Vasselier, Abigael, “Updating the EU strategy on China: co-existence while de-risking through partnerships”, Bruegel, October 2024, https://www.bruegel.org/sites/default/files/2024-10/PB%2027%202024%20311024.pdf

[27] García-Herrero, Alicia, “The EU’s concept of de-risking hovers around economic diversification rather than national security”, Bruegel, 6 December 2023, https://www.bruegel.org/sites/default/files/2024-07/The%20EU%E2%80%99s%20concept%20of%20de-risking%20hovers%20around%20economic%20diversification%20rather%20than%20national%20security.pdf

[28] Fleck, Jörn, Lipsky, Josh, and Shullman, David O., “Ursula von der Leyen set Europe’s ‘de-risking’ in motion. What’s the status one year later?”, New Atlanticist, 7 April 2024, https://www.atlanticcouncil.org/blogs/new-atlanticist/ursula-von-der-leyen-set-europes-de-risking-in-motion-whats-the-status-one-year-later/