Home>Innovative Financing Schemes

23 August 2023

Innovative Financing Schemes

By Theresa Jahr

Introduction

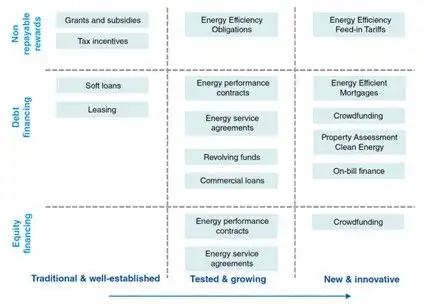

The European Commission estimates a gap in investments in energy efficiency (EE) to achieve its set targets of around €165 billion (European Commission, 2021a). This lack of investment is due to various reasons, including the perception of high upfront costs, lack of awareness and information, and various market and regulatory barriers. Numerous financial instruments are being used to try to close this gap and help overcome these barriers. Such instruments can be divided into three types depending on their market saturation in Europeas done in Figure 1 (Bertoldi et. al., 2020). There are traditional financing instruments such as grants, subsidies, tax incentives, and loans. These have already been operating for several decades across many EU Member States. However, due to the persistent investment gap, these are arguably not sufficient on their own to bridge it. Next, there are tested and growing instruments such as energy performance contracts and energy service agreements. These have been proven to work in several EU Member States, and are becoming increasingly significant in scale with more widespread applications. Lastly, there are new and innovative schemes, that have little to no application in the EU so far but haveoften already been tried out in other parts of the world. These instruments hold the potential to improve EE financing and tackle problems that traditional and growing ones cannot. I will focus on these innovative financing schemes in this paper. Due to the limited scope of the paper, I will discuss two innovative schemes in particular: on-bill and on-tax financing schemes.

In the next section, I will first introduce the concepts of on-bill and on-tax financing. The following section will consider if such schemes have been implemented in other parts of the world, or even in the EU already. Lastly, it will discuss the possibilities and limitations of the EU implementation.

Innovative Financing Schemes: On-Bill and On-Tax Financing Schemes

First, I will consider the on-bill financing (OBF) mechanism. This mechanism links repayment of EE investments to the utility bill and thereby allows building owners to repay the cost of energy efficiency upgrades through their utility bills over time. This lowers the high upfront investment cost barriers that owners often face and can tackle split incentives barriers. The funds used to support these investments can originate from utilities, the state, or third parties including commercial banks. For the on-bill financing to be effective, the energy savings arising from the newly installed EE measures must be large enough so that the total post-renovation utility bill does not exceed the pre-renovation bill (Henderson, 2012). If this is the case, the customer sees an immediate net reduction in their energy costs. OBF mechanisms can be divided into on-bill loans and on-bill tariffs. In the former, the money is borrowed from a third-party lender and is paid back through the utility bill. The loan is separate from the customer’s regular utility charges and may thus come with interest charges or fees. The latter allows customers to pay for EE improvements through a tariff on their utility bill which is often directly offered by the utility company. One key difference between the two is that on-bill loans must be paid off in case of ownership transfer, whereas on-bill tariffs assign the obligation to the property itself and therefore allows for a transfer of the repayments to the next tenant or buyer (Jewell, 2009). OBF mechanisms are also sometimes referred to as pay-as-you-save schemes (PAYS) because customers pay for the upgrades using the savings they achieve on their energy bills, as is the case for on-bill loans and on-bill tariffs.

On-tax financing (OTF) allows building owners to repay the cost of energy efficiency upgrades through their property taxes over a long-term period. This is also called property-assessed clean energy financing (PACE). Hereby, the local government provides the upfront funding for the energy efficiency project, and the building owner repays the loan through an additional charge on their property tax bill based on an annual assessment. This repayment via taxation by a public authority is what makes the mechanism innovative. The repayment amount is usually lower than the savings generated by the project, so the building owner sees immediate savings on their energy bill. PACE assessments are transferrable, meaning the investments can be recovered when the property is sold, resulting in less concern about investment recovery during sale transactions. Furthermore, PACE programs are appealing to lenders since they are secured by a senior lien on the owner’s property, which separates repayment security from the borrower’s creditworthiness (Headen et al., 2011). Both OBF and OTF can overcome some of the barriers to EE investments, such as high upfront costs, limited access to financing, and split incentives. They thereby have the potential to accelerate the uptake of EE measures for SMEs, who typically struggle with these barriers.

Their Application

Utility OBF programs have been used in the US for many years, with capital sources ranging from bond issues, public loan funds, revenue from cap and trade programs, banks, credit unions, and capital markets (Bell et al., 2011). A specific example is Southern California Edison (SCE), which provides business, institutional, and government customers with a no-fee, interest-free loan that is repaid using the expected energy savings from the SCE electricity bill (Jawell, 2010). Experience from the US shows that even if OBF has the potential to solve problems such as upfront costs and split incentives, significant issues still need to be resolved. Among those issues are the need to modify billing systems, the identification risks of no payment cases and the diversification of capital sources. Johnson et al. (2012) identify some elements for the successful deployment of OBF in residential buildings by contrasting the on-bill programs created by two utilities, Midwest Energy and Hawaiian Electric Company. They found that simple application procedures, positive working relationships with the contractors, shared advantages for all parties concerned, and flexibility in terms and conditions are crucial for the success of OBFs.

There are some examples of OBFs implemented in the EU. The first PAYS-inspired scheme was implemented by the UK in 2013 as part of the Green Deal (Rosenow and Eyre, 2013)[1]. It gave owners and occupants the possibility to install EE improvements at no up-front cost. However, the UK scheme did not function as well as anticipated and public funding ended in 2015. A number of factors are said to have contributed to its failure such as a high interest rate attached to the loan, the attachment of the loan with the property rather than the occupant and, instead of using figures based on the occupant’s energy usage, loan repayments were calculated using average predicted figures (Mundaca and Kloke, 2018).

Another European example is the “Better Energy Finance” scheme, a government-funded initiative launched in Ireland in 2015 based on the idea of a market-based PAYS. It was designed to provide affordable financing options for homeowners to make energy-efficient upgrades to their homes by providing low-interest loans. However, despite several differences and perceived improvements to the UK example, the Irish scheme did not gain momentum either.

On-tax PACE initiatives are most widely established in the US. 36 US states had PACE-enabling legislation in 2020, of which 12 had running programs, while others were developing them (Bertoldi et. al., 2020). The experience in the US shows that there can be several problems with PACE financing when not properly designed and administrated. On the one hand, because PACE financing is structured as a tax assessment instead of a loan, PACE programs do not have to provide homeowners with the same disclosures about the financing costs that traditional lenders must provide. Homeowners have complained that PACE contractors are lying about the costs of financing as part of selling the program. And on the other hand, because the financing is designed to stay with the property, the eligibility of the homeowner is based primarily on property information rather than income and FICO scores. Together, these problems can create a situation in which homeowners suddenly owe far more in property taxes than they can afford to repay (Cox, 2011). Another problem is that interest rates for PACE programs are usually 3-4% higher than for traditional mortgage loans (ibid.). Moreover, some buyers and sellers have had difficulty with the sales of homes with PACE tax assessments.

In the EU, the pilot project EuroPACE as part of the European Commission’s Horizon 2020 program has tested the concept in a municipality in Spain (European Commission, 2021b). It adopted best practices from the US PACE market and intended to further enhance its impact. EuroPACE mobilised both private capital and public funds and combined the PACE concept with a one-stop shop. One-stop shops are advisors that offer services that cover the whole, or at least the majority of the renovation value chain. The EuroPACE project is said to have overcome the main barriers to home renovation and while it stopped in 2021, it has inspired other EU projects such as Save the Homes, FITHOME, HIROSS4all, and the HolaDomus in Barcelona (CASE, 2021). Furthermore, a PACE project is being developed on the Balearic Islands as part of the Horizon 2020-funded REGENERATE project.

Discussion

Regarding on-bill financing schemes, complex design elements, the requirement for additional regulation to enable repayment charges on the utility bill, and the establishment of fully liberalized EU energy markets with several suppliers being hesitant to participate are some of the difficulties that can explain why OBF instruments have not yet been successfully implemented in the EU. It is also important to keep in mind that OBF instruments compete with a variety of other EU financing instruments, many of which have more appealing conditions than OBFs, such as grants, low-interest loans, and tax advantages (Bertoldi et. al., 2020). Nevertheless, if these shortcomings and limitations were to be addressed and worked out, on-bill financing might be able to significantly benefit the uptake of EE measures in the EU as it does in the US. Bell et. al. (2011) point out that on-bill financing schemes provide a significant opportunity especially for small businesses, due to the simple procedure, the credibility of utility measurement and verification program to assure that the project will deliver the energy savings it promises and the immediate financial benefit it offers. According to Mundaca and Kloke (2018), properly crafted OBF schemes have the ability to successfully enable investments and raise the attractiveness of these investments for energy consumers. However, they argue that given the complexity of the EE markets and the challenges posed by on-bill financing schemes to utilities’ primary business, more legislative interventions are required.

Complicated legal procedures and issues with first-lien are said to be impediments to EU application of PACE schemes that must first be resolved for their successful application. Also, PACE is typically based on municipal bonds, which are uncommon in EU cities, particularly small ones. Nevertheless, we saw that there are several applications in the EU and their popularity is growing. More research would need to be done to assess whether the negative effects seen in the US are also the case in the EU.

To sum up, both on-bill and on-tax financing have had extensive applications in the US and are currently being tried out in the context of the EU. While shortcomings and barriers remain, there is a potential for both to be further developed and applied in the EU context.

Bibliography

- Bell, C., Nadel, S. and S. Hayes (2011), ‘On-bill financing for energy efficiency improvements: A review of current program challenges, opportunities and best practices’, Washington, D.C.: American Council for an Energy Efficient Economy.

- Bertoldi, P., M. Economidou, V. Palermo, B. Boza-Kiss and V. Todeschi (2020), ‘How to finance energy renovation of residential buildings: Review of current and emerging financing instruments in the EU’, WIREs Energy and Environment, Vol. 10(3). https://doi.org/10.1002/wene.384

- Brown, M. H. (2009), ‘On-Bill Financing: Helping Small Businesses Reduce Emissions and Energy Use While Improving Profitability’, Washington, D.C.: National Small Business Association.

- CASE (2021), ‘Farewell EuroPACE’, Accessed on 31st of March, 2023, at: https://www.case-research.eu/en/farewell-europace-101858

- Cox, P. (2011), ‘Keeping PACE?: The Case Against Property Assessed Clean Energy Financing Programs’, University of Colorado Law Review, Vol. 83, pp. 109–113.

- European Commission (2021a) “Impact assessment report accompanying Proposal for a Directive of the European Parliament and of the Council on energy efficiency (recast)”, Commission Staff Working Document, Brussels, SWD(2021) 623 final.

- European Commission (2021b), ‘Developing, piloting and standardising on-tax financing for residential energy efficiency retrofits in European cities’, Accessed on 31st of March, 2023, at: https://cordis.europa.eu/article/id/422271-a-home-based-financing-model-to-boost-investments-in-sustainable-renovation

- Headen, R. C., S.W. Bloomfield, M. Warnock and C. Bell (2011), ‘Property assessed clean energy financing: The Ohio story’, The Electricity Journal, Vol. 24, pp. 47–56. https://doi.org/10.1016/j.tej.2010.11.004

- Henderson, P. (2012), ‘On-bill financing overview and key considerations for program design’, New York: Natural Resources Defense Council.

- Jewell, M. (2009), ‘The growing popularity of on-bill financing’, Engineered Systems, Vol. 26(9), pp.18–20.

- Jewell, M. (2010), ‘Efficiency incentives: Incentive funding continues to grow’, Engineered Systems, Vol. 27(9), pp. 21–22.

- Johnson, K., G. Willoughby, W. Shimoda and M. Volker (2012), ‘Lessons learned from the field: Key strategies for implementing successful on-the-bill financing programs’ Energy Efficiency, Vol. 5(1), pp. 109–119.

- Kirkpatrick, A. J. and L.S. Bennear (2014), ‘Promoting clean energy investment: An empirical analysis of property assessed clean energy’, Journal of Environmental Economics and Management, Vol. 68, pp. 357–375. https://doi.org/10.1016/j.jeem.2014.05.001

- Mundaca, L., & Kloke, S. (2018), ‘On-bill financing programs to support low-carbon energy technologies: An agent-oriented assessment’, Review of Policy Research, Vol. 35, pp. 502–537. https://doi.org/10.1111/ropr.12302

- Rosenow, J. and N. Eyre (2013), ‘The Green Deal and the Energy Company Obligation’, Energy, Vol.166(3), pp. 127–136.