Home>US yields on the rise: back to 2013?

03.03.2021

US yields on the rise: back to 2013?

From a historic low of 0.5% back in August 2020, 10-year US Treasury yields have climbed up to 1.5% in recent weeks; at the same time, market-based inflation expectations also reached their highest levels in the last decade. This feeds into the broader debate around inflation expectations, the speed of the recovery and the evolution of US monetary policy. We asked Nicolas Goetzmann, Head of Research and Macroeconomic Strategy at la Financière de la Cité, to share his thoughts on those movements and the risk of another “taper tantrum” as happened in 2013, when fears of monetary tightening led to sharp yields rises.

What are the drivers behind the recent evolution of US treasury yields?

First, it is important to debunk the usual narrative which indicates that “Monetary policy artificially depresses yields”. Interest rate cuts and quantitative easing are supposed to support aggregate demand – inflation and growth anticipations – that will push yields higher eventually. In this logic, Mario Draghi said, in September 2016(1) “interest rates have to be low today to be high tomorrow.”

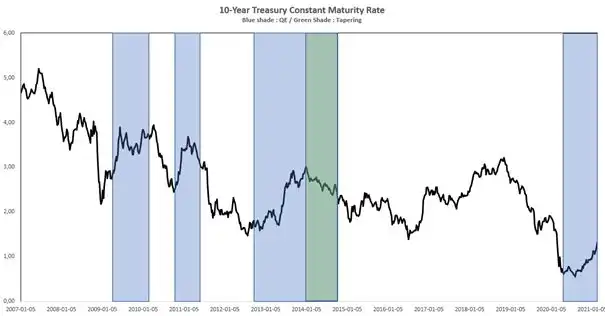

Eventually, nominal growth drives yields, lower or higher, depending on expectations. Paradoxically enough, a tight monetary policy could drive yields lower whereas an accommodative monetary policy stance could do the opposite. As we can see below, the last rounds of QE came when yields were falling – as a sign of weaker nominal growth forecasts – and pushed them higher through stronger forecasts due to an active monetary policy. QE was therefore highly efficient.

The current surge in US yields is the direct result of the Fed’s intervention and must be seen positively. On February 23, Jerome Powell said “In a way it’s a statement of confidence on the part of markets that we will have a robust recovery”(2).

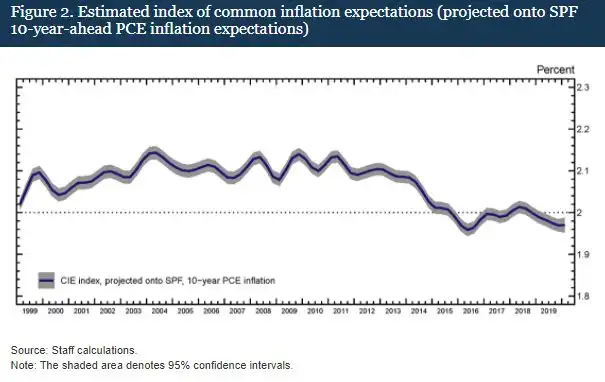

Interestingly, we have seen the 10-year breakeven inflation rate come back to a level not seen since August 2014. This surge in inflation expectations reversed not only the recent collapse in yields following the pandemic, but also the inflation expectations decline of the previous years. As breakeven rates are not considered a perfect tool for inflation expectations, on September 2, the Federal Reserve published the Index of Common Inflation Expectations (CIE index)(3) as a better alternative.

According to Goldman Sachs calculations, as in the case of the 10-year breakeven inflation rate, the CIE index also came back to its 2014 level in the last days of February 2021.

Thus, the recent surge in inflation expectations – as a component of US yields – is not only conjunctural, but also structural. This situation could be explained by the August 27 monetary policy review with which the Federal Reserve halted Inflation Targeting (IT) to adopt a new “Flexible Average Inflation Targeting” (FAIT) strategy. This new framework allows the Federal Reserve to overshoot the inflation target for a while, to get back to maximum employment as fast as possible. As Inflation Targeting has been indicated as a cause of the fall in inflation expectations since 2012 – when the Federal Reserve chose to adopt this strategy (January 2012) – the monetary policy review and the new FAIT strategy are clearing the gap that developed since 2012.

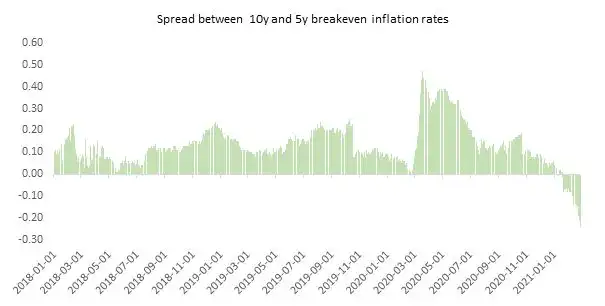

The credibility of the new framework is demonstrated by the current inversion of breakeven rate curve. As the Fed committed to overshoot its target in the medium term, 5-year breakeven inflation rates are now higher than their 10-year counterpart. This is precisely what the Fed is pursuing: having inflation above target in the short-term – hence high 5-year inflation expectations – and at or below the target in the medium- to long-term – hence lower expected inflation between 5 and 10 years from now.

Moreover, the inversion of the 5-10 years inflation expectations curve is highlighting the Federal Reserve’s credibility in the matter of controlling inflation in the long term.

Overall, the current surge in US interest rates is a sign of higher growth and inflation expectations, which is healthy. It is also a sign of a structural move in the Fed’s framework, which could be a trigger for stronger growth in this decade, compared to the 2010s.

Should we worry about a new “taper tantrum”? What should be the impact for emerging markets?

Chile has a strong commitment on climate action. The Ministry of Finance has led several initiatives on green finance, becoming the first sovereign in the Americas to issue green bonds, co-chairing the Coalition of Finance Ministers for Climate Action, publishing our Financial Strategy on Climate Change, among others.

Since the first issuance in June-2019, we have issued roughly USD7.7 billion in green bonds. The main motivation to issue green bonds was to demonstrate our commitment on climate action, while at the same time further diversify our investor base. We are proud to mention that these issuances broke with conventional wisdom, as they demonstrated that one can take concrete steps on climate action and also achieve important financial gains, both in terms of low yields and investor diversification.

We have also stepped up our efforts to engage with investors. First, we had special investor roadshows in Europe, Asia, and North America to describe our Green Bond Framework and present Chile’s overall credentials and efforts related to climate action. We have complemented these efforts with documentation with answers to frequently answered questions, presentations that describe the certified project portfolios and issuance results. In line with international best practice, we published our Green Bond Impact and Allocation Report last year, and are set to publish a new version in the next few months. Updates on our efforts are also disseminated in the investor community with regular newsletters sent out to our investor base. Finally, we actively give interviews to the local and regional financial press, participate in seminars and panels to disseminate knowledge, foster greater visibility of green bonds, and contribute towards a faster development of the green asset class.