ASEAN’s Energy Security Challenges

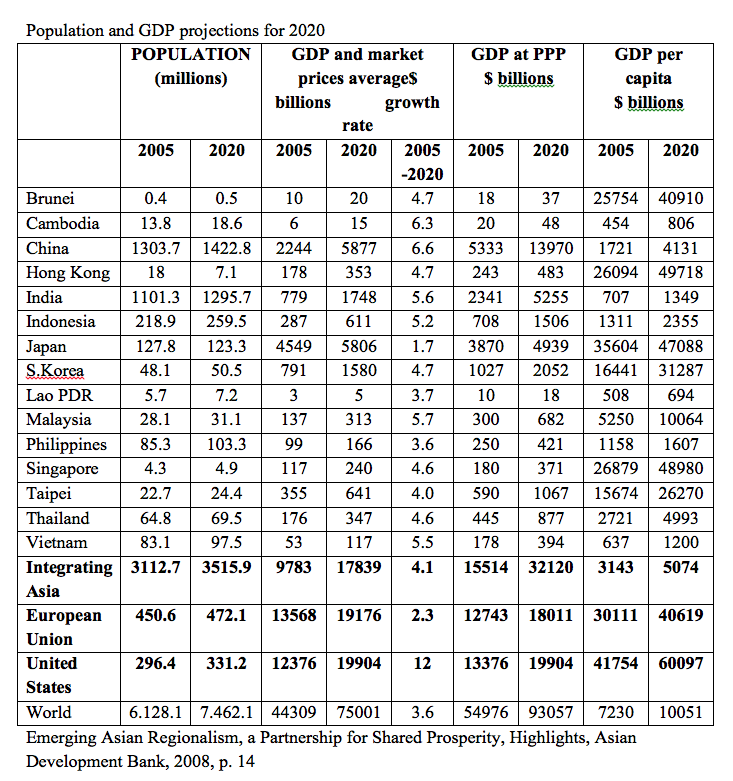

Asia has experienced remarkable economic growth rates over the past 3 decades. Average income in the 1990s increased by about 7 percent, accelerating to 8.5 percent in the years 2000-2010 as the giant economies of China and India posted robust growth. Average economic growth in developing Asia is expected to remain in the 6-7 percent range over the remainder of the decade. Such rapid pace of development has also been highly energy intensive. While in 2010 its GDP was 28 percent of global GDP, Asia’s energy use was 34 percent of global use (ADB 2011). Hence Asia’s growth has been highly energy intensive. As Asia’s per capita income continues to rise at a brisk pace of the next decades and the middle income class expands rapidly, demand for modern energy sources is also be expected to intensify.

Asia is a relatively energy poor region, particularly with respect to oil. Projections to 2035 show that Asia will produce less than half its energy needs while representing nearly half the world GDP (ADB 2011). This is obviously a very worrisome perspective. Many countries will only produce a fraction of their needs. In the middle of Asia and surrounded by the energy deficient giant economies of China and India, ASEAN is overall an energy surplus area but the energy endowment of its countries differs very much with countries such as Thailand, the Philippines, Singapore and Viet Nam being large energy deficient countries while Lao PDR, Malaysia and Indonesia are in better position. By 2035 however, except for Brunei, all ASEAN countries will be energy deficient.

For ASEAN, the energy issue represents a huge challenge on many fronts.

First internally and externally, energy will be a major challenge to ASEAN integration itself as it can either push the countries towards strong regional unity and integration or it can push them apart.

Second, externally, energy demand from China in particular, but possibly also from India, will put competitive pressure on ASEAN unity. Some ASEAN countries might prefer trading with non-ASEAN countries rather than within ASEAN.

Third, larger border areas of ASEAN particularly offshore have overlapping claims by both ASEAN and non-ASEAN countries. These sovereignty issues pose a serious threat to ASEAN unity and integration itself. Internally, again, many internal ASEAN borders are not defined, including in many areas where energy sources may be present.

Besides resources availability, energy efficiency and conservation –in the context of growing populist policies- , environmental sustainability in particular in hydropower development and energy trade are all areas which could benefit from stronger ASEAN cooperation and integration but could also be sources of disagreement and rivalry.

Table 1

Economic Development and Energy in Asia and ASEAN, 2030-2050

Rapid economic growth in Asia has led to a sharp rise in energy consumption. Asia accounted for 20 percent of world energy consumption in 2000, rising to 34 percent by 2010 and projected to rise a huge 51 percent by 2035 based on rather optimistic assumptions on improved energy efficiency (ADB 2011 and ADB 2013). Historically from 1990 to 2000, energy efficiency improved on average by 2.47%, while the more optimistic assumption to 2035 assumes a 3.2% gain. Even under this assumption, energy consumption will double in Asia between 2010 and 2035 (ADB 2013). Most organizations project primary energy use in Asia to grow by about 2.8% over this period. Table 1 summaries energy demand and supply derived from an ADB study on long term perspectives for Asia (ADB 2011).

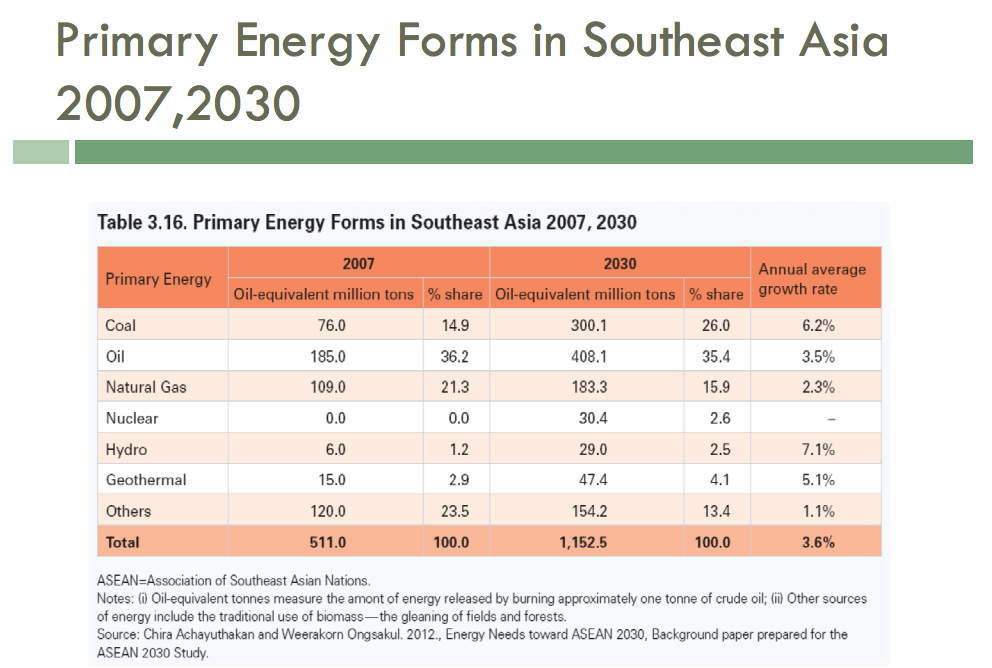

Looking forward, the issue is not only total energy demand as such but also the composition of demand. A per capita incomes increase Asians will use more cars requiring transportable fuel and air conditioning or heating which will require more electricity generation. For Asia as a whole, fossil fuels will continue to be the main source of primary energy. Recent studies show that oil consumption will double over the 2010-2035 period, natural gas use will more than triple while coal consumption could rise by over 80% (ADB 2013). Hydropower is expected to quadruple. In 2010, Asia’s hydropower capacity was 337 GW. All renewables (hydropower, wind, solar, bio-fuels, geothermal) will increase but account for only a small 13% of power generation mix by 2035. Similarly nuclear energy is expected to also remain small. Energy mixes will however differ significantly across different parts of Asia. South Asia and East Asia for instance will be large users of coal while Central Asia has ample natural gas reserves. Projections for ASEAN show a relatively balanced demand for various types of primary energy, with oil demand appearing to increase somewhat more rapidly. Overall ASEAN currently relies on fossil fuels for 73% of its energy.

http://www.eia.gov/todayinenergy/detail.cfm?id=4390

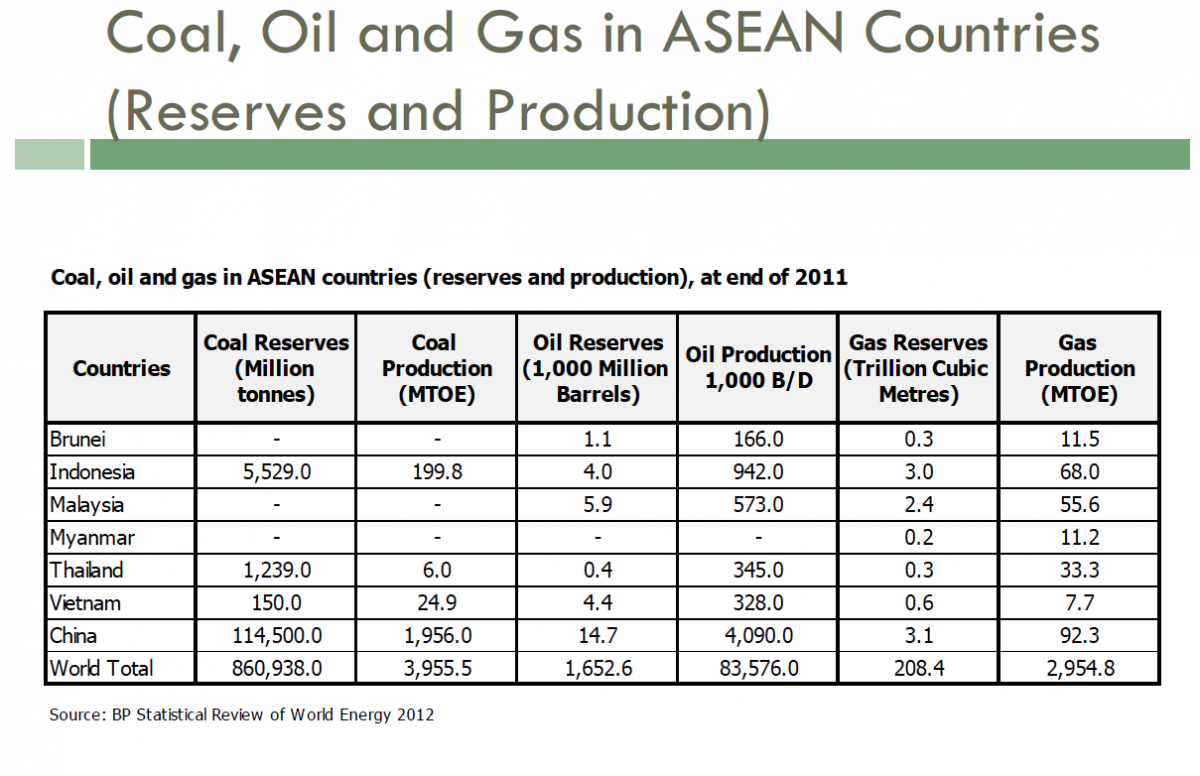

Given these broad demand projections, it is important to look at the supply side to get a better understanding of Asia’s energy security future issues, and in particular the security questions ASEAN will face. Overall, Asia is well endowed with coal, possessing 35% of world reserves, and with natural gas where it has roughly 16% of world resources. Also trade in coal and natural gas is well developed and diversified worldwide. Asia hydropower potential is five time current capacity, as high as 1,700 GW (ADB 2013). In contrast Asia possesses less than 10% of world oil reserves. With oil consumption projected to increase rapidly in Asia, the region is highly vulnerable to oil market disruptions. In 2010, Asia accounted for about half of the world oil imports or 11 million barrels per day. Asia uses nearly half its oil for motor vehicles. With rapid growth projected in per capita incomes, particularly in China and India, demand for oil in transportation will increase rapidly. In China alone, the road vehicle fleet is forecast to grow by more than 6% annually over the next 20 years. While there is some possibility of substitution with biofuels and liquid natural gas, pending a major technological breakthrough, oil will remain the main fuel used in transportation. Asia’s oil imports are projected to grow by about 4.2% annually and reach more than 31 million barrels per day by 2035.

Asia’s vital dependence on oil imports which will only intensify over the next few decades is at the core of Asia energy security challenge, and explains why the rivalry over many overlapping land and maritime areas which might contain oil or gas reserves poses serious security threats to Asia. Bordered on land and at sea by two of the largest and fastest growing economies in the world highly depending on oil imports, ASEAN is in a particularly delicate strategic position. Although most ASEAN countries except Singapore are relatively well endowed with energy resources, all of them except Brunei will no longer be energy self sufficient in 20 years time. More importantly all ASEAN’s oil will need to be imported.

Given developments in the energy sector in recent years with respect to the development of unconventional gas namely shale gas and coal bed methane, there is a possibility that the energy situation in Asia might change substantially over the next 2 decades. It looks like China might hold about 20% of the world shale gas resources while Indonesia’s potential is put at 8.7 GToe. India and Pakistan are also estimated to have significant shale gas reserves. Indonesia might have the largest world coal bed methane resources followed by China. Some estimates put Indonesia’s recoverable reserves at 1,300 GToe -one third of its conventional gas reserves- (ADB 2013). All these estimates while promising are very preliminary. The particular geological situations and the density of population might make exploitations of the unconventional gas resources not feasible or too costly in many cases. Still as shown in North America rapid changes could occur.

ASEAN

In 2010, ASEAN remained and energy surplus region. As shown in table 2, the region has substantial and diversified energy resources ranging from fossil fuels, hydropower, geothermal, bio-fuels and biomass and solar. Brunei, Indonesia, Malaysia, Myanmar and Viet Nam have significant oil and gas reserves. Cambodia has the geological potential for oil and gas reserves. Chevron, the US conglomerate, has active in exploring several off shore blocks of oil. Total reserves remain however uncertain and production has been postponed several times and is currently scheduled not before 2016. Similarly many areas offshore and onshore in Myanmar have not been explored yet, but hold good potential. Currently Myanmar’s proven reserves are only half those of Viet Nam, with good potential to at least reach the level of Viet Nam of 0.6 trillion cubic meters of gas. There is also some possibility of oil or gas reserves in the South of Laos.

Table 2

Source : Les enjeux de la question énergétique en Asie et dans l'ASEAN, Jean-Pierre Verbiest, 16 novembre 2012.

Finally, there is also speculation that parts of the South China Sea area might contain vast oil and gas reserves. Much of the area is of course contested by several regional countries. Overall however, ASEAN’s oil reserves are quite small compared to other region in the world. As shown in figure 1, except for Brunei and Malaysia, all other ASEAN countries are already oil importers. Gas reserves are significant in Indonesia and Malaysia. Although tiny compared to China, coal reserves are important in Indonesia, Thailand and Viet Nam.

Table 3

Source : Les enjeux de la question énergétique en Asie et dans l'ASEAN, Jean-Pierre Verbiest, 16 novembre 2012.

Given its abundant water resources and large river basins, ASEAN has substantial hydropower capacity. The GMS region alone has a capacity of 250,000 MW, half of it feasible. The lower Mekong Basin has potential between 50,000 and 64,000 MW. Overall only 6000 MW have been built so far. Viet Nam has actual potential for 20,000 MW, Laos 26,500 MW, Cambodia 10,000 MW and Myanmar 25,000 MW. Substantial potential also exists in Sarawak, Malaysia, Indonesia and the Philippines. While the potential for hydropower development in ASEAN remains huge, resistance by civil society related to environmental concerns has been growing in most ASEAN countries. Concerns are also rising as to the impact of changing weather patterns on hydropower availability. Hence a strategy of major reliance on hydropower for electricity generation is considered highly risky. Geothermal power has a huge potential in Indonesia and the Philippines, countries which are part of the Ring of Fire. Indonesia has the largest potential in the world estimated at 28 Giga Watt (22,000 MW) with only 1.194 Giga Watt utilized (WWF, Igniting the Ring of Fire, 2012). However, much of it is located in outer islands and might not be economically exploitable. The Philippines is the second largest geothermal energy producer in the world, with 1.8 GW installed capacity producing over 17% of its electricity. Its capacity is estimated at 4500 MW with production reaching over 12,000 GWh by 2022. While the potential is there, geothermal power requires large upfront risky investments in drilling and plant development. Its viability obviously depends on government tariff policies to reduce CO2 emissions. As mentioned above, Indonesia by far the largest and most populated country of ASEAN might have substantial reserves of non conventional gas.

ASEAN countries have good potential in other renewable energy sources, namely biomass and solar. Laos, Myanmar and Thailand can also produce significant amount of bio-fuels without threatening food production. All these sources of energy will however remain relatively small compared to conventional sources.

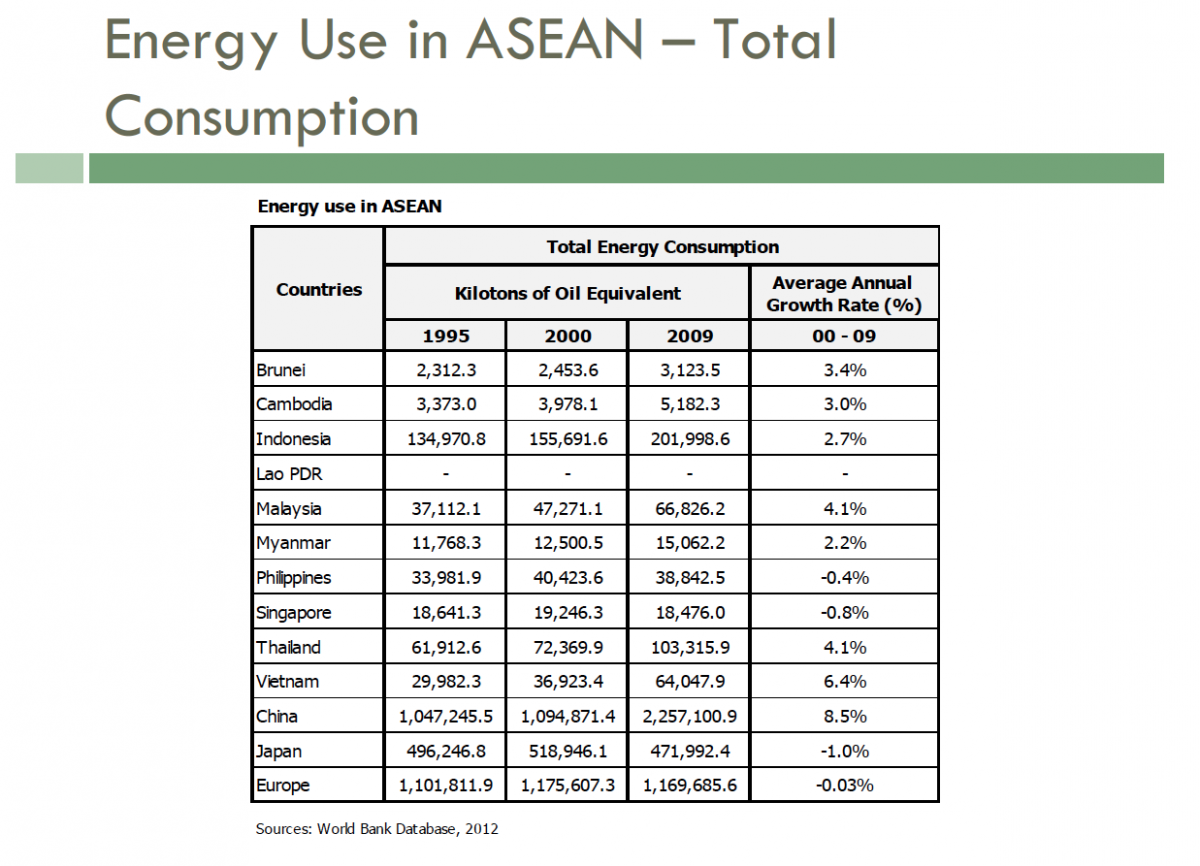

As shown above, while ASEAN is a relatively well endowed region in terms of energy resources, it is however an energy thirsty region with low energy efficiency as its transport sector and its manufacturing industry is highly energy intensive. Table 4 (tables below to be merged) shows energy consumption for ASEAN countries. Over the past decade, most ASEAN countries except the Philippines and Singapore have experienced rapid growth in energy consumption per capita. For instance, Indonesia with an economy growing at a modest rate of 6% in 2009-2010, experience a 9% jump in electricity demand.

Table 4

Source : Les enjeux de la question énergétique en Asie et dans l'ASEAN, Jean-Pierre Verbiest, 16 novembre 2012.

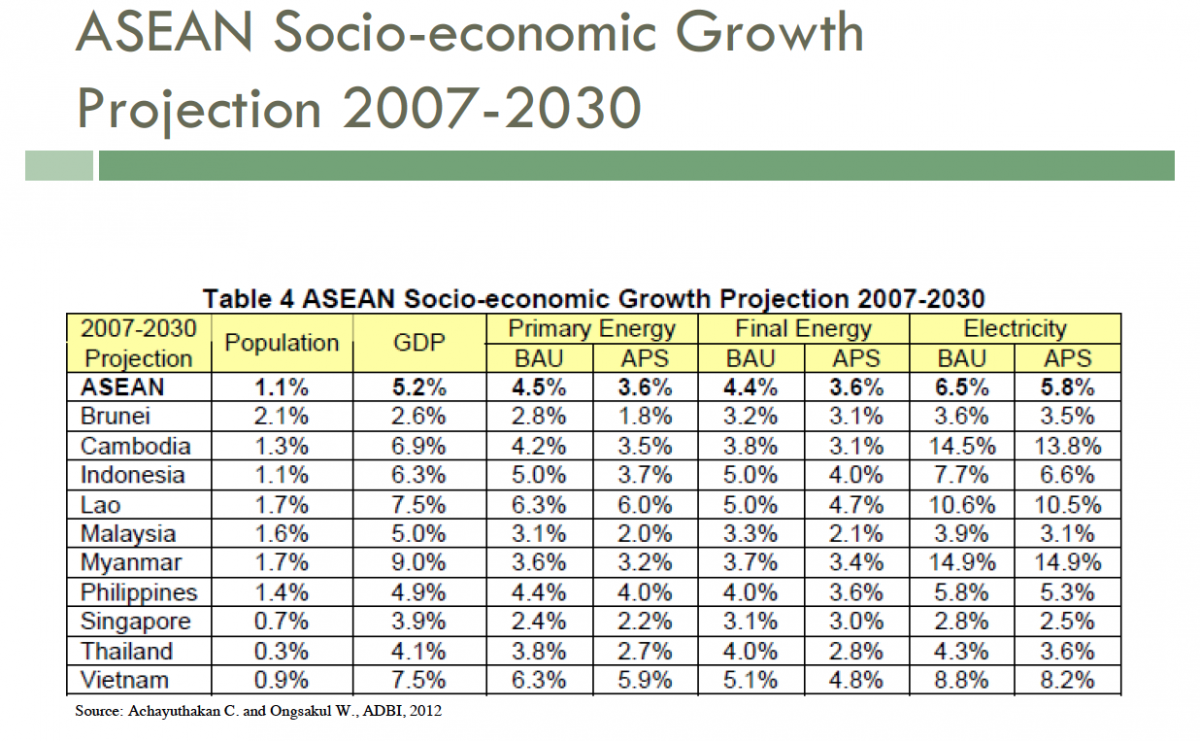

Table 4 shows primary and final energy consumption projections to 2030 (ADBI 2013). The BAU projections are business as usual while under the alternative policy scenario (APS) energy savings and reduced CO2 emissions are factored in. Both primary and final energy use under both scenarios generally grows slower than GDP implying some improvement in energy efficiency. Electricity use is projected to increase much faster than GDP as per capita income increases and electricity is more widely used. Depending on the energy resources endowments of each ASEAN country, such rapid rise in electricity use will have different implications on primary energy use, but in general coal and hydropower will become more important sources of electricity production, particularly in Indonesia, Malaysia, the Philippines, Thailand and Viet Nam.

Table 5

Source : Les enjeux de la question énergétique en Asie et dans l'ASEAN, Jean-Pierre Verbiest, 16 novembre 2012.

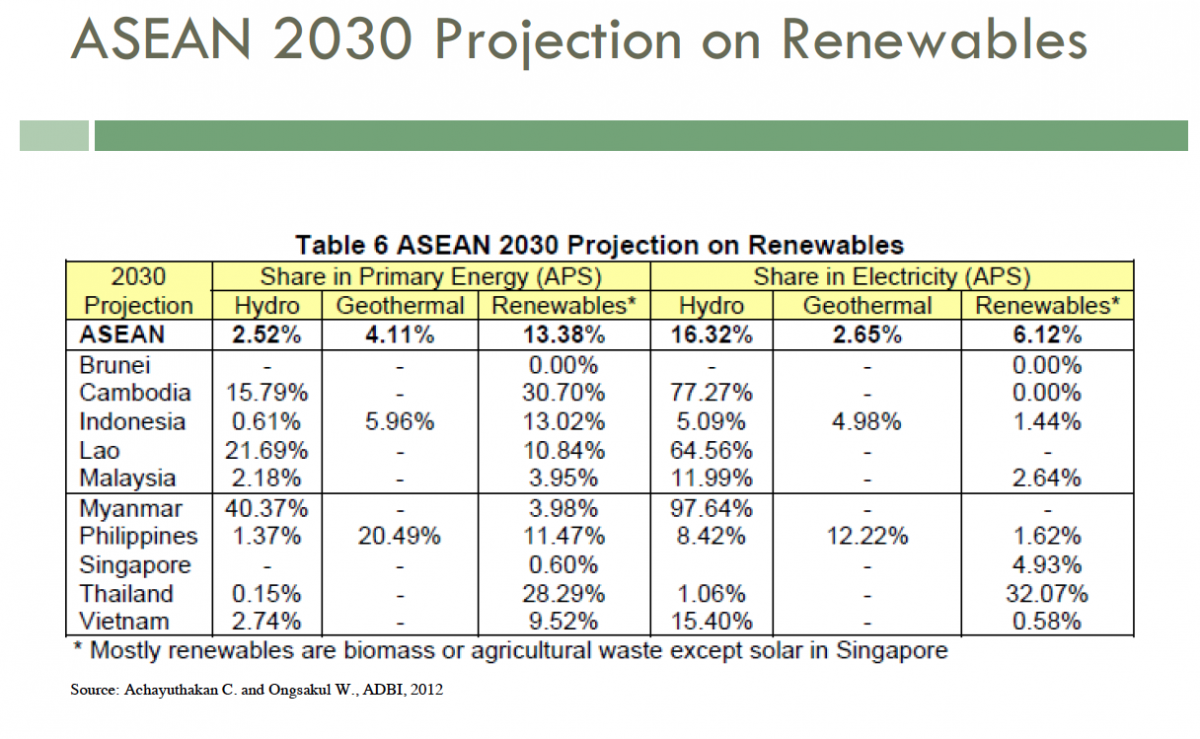

Table 6 shows the share of renewable in primary energy and in electricity production. Although overall their share in the energy equation of ASEAN is rather small, for some of the countries hydropower could become important for electricity production.

Table 6

Source : Les enjeux de la question énergétique en Asie et dans l'ASEAN, Jean-Pierre Verbiest, 16 novembre 2012.

Even under the most optimistic assumptions, the above analysis clearly shows that ASEAN is facing formidable challenges in securing the energy it will need over the next few decades to sustain its growth momentum. Many of ASEAN’s current fossil fuel reserves will be exhausted or far from sufficient to respond to projected demand. Except for Brunei, by 2035, all ASEAN countries will be far from energy self sufficiency, even countries with relatively large current reserves such as Malaysia and Myanmar (ADB 2030). Ensuring access to sufficient energy supply of the right type at affordable cost while mitigating the environmental impact of energy production will be a major challenge for ASEAN, not the least because it is itself surrounded by 2 massive economies also short of energy resources. To address this challenge, strong domestic and regional political leadership will be required.

Due to the increasing energy demand from all the participants of the Asean, any alternative source is acutely considered. The issue becomes dramatic as soon as China is implied in the game, and China always takes part to this harsh competition for energy supply in Southeast Asia. Because of its size, its economic, financial and military capacities, the great Northern Neighbor is able to exert hegemony that ASEAN cannot contest. The question is to know whether the diplomacy of non interference in accordance with ASEAN principles suffices to stabilize a very sensible situation on the long term.